Page

Situations Affected By Financial Trends

Completion requirements

View

Investments

Click here to view a video that explains investments.

Money that is put away into a savings scheme so that it can:

- Grow and become more than the original amount

- Earn interest so that the money grows

An investment can be for a:

- Short term = less than 6 months

- Medium-term = 6 to 36 months

- Long term = more than 36 months

The basic principle for any investment is: “the higher the return, the higher the risk’

What this means is that the more interest they promise you on an investment, the higher the risk is for you (the investor) to invest your money.

A good example of a risky investment would be if you invest money in the stock market i.e. buying and selling shares. If you do not know what is going on, when to buy, when to sell, you could end up losing all your money. However, if you know what is going on in the stock market and you can ‘read between the lines, you will make much more money than you invested.

Safer investments usually bear a lower interest rate. A fixed deposit is a good example of a safe investment. You know your money is going nowhere and it will still be there at the end of your investment period

Unit trusts are less risky, but they are a long-term investment. Unit trusts are offered by financial institutions that collect amounts of money from many people. These institutions employ people who know the stock market very well and they are called fund managers. These fund managers buy blue-chip (safe and stable) shares with this collective amount of money. The value of the shares is then equally distributed amongst the initial payers. When you ‘sell’ your unit trust back to the financial institution, your return on investment includes dividends and interest.

Dividends are money that is made from buying and selling the shares and interest is the return on the money that you invested.

Unit trusts can be up one day and down the next, so you still need to be very careful about when you buy or sell. The rule is to buy when the stock market is down and sell when it is up. Timing is very important.

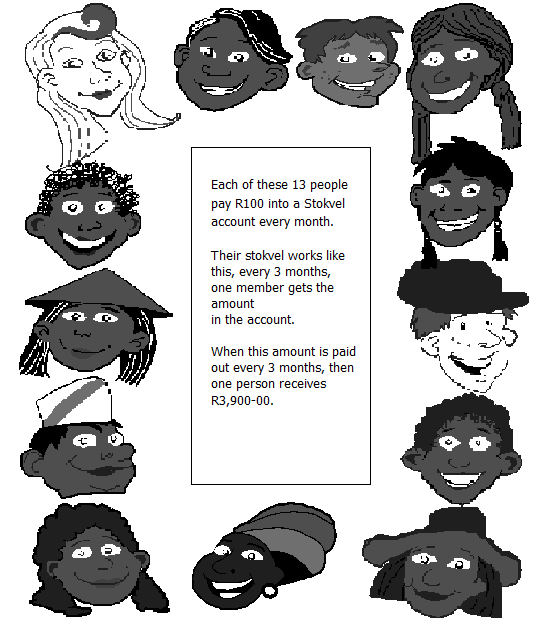

Stokvels

A stokvel is usually when a number of people get together and ‘club’ together with their money. Every member of the stokvel receives the money at a particular time.

Because a number of people contribute, the money and interest accumulate more rapidly than if you were saving on your own.

Inflation

Inflation is the average change in prices over a period of time. We often hear what the inflation rate is when we listen to financial reports over the radio.

If our inflation rate is 15%, then it means that this time last year something that cost R100-00 will now cost you R100-00 + 15% = R115-00.

Inflation can be a vicious wealth killer.

Example:

Piet works at Hummingbird Milling. Piet wastes a lot of mealiemeal every day, because he is not interested in his work. The company loses money. At the end of the year, they take a big knock for all Piet’s wasting of mealiemeal. This means less profit. Less profit mean less money in the bank.

Less money in the bank means less increase for staff. Less increase for staff means less comfort at home. Less comfort at home makes more miserable people. More miserable people become unhappier at work. Unhappy workers become less interested in what they do. Less interest becomes more waste.

Hummingbird Milling knows all this and decides to put up the prices of their mealiemeal to compensate for Piet’s lack of interest. They put the mealiemeal price up by R1-00. The stores that sell mealiemeal to the public have to put up their prices and they do so by making mealiemeal R2-00 more expensive.

If this happens every day and everywhere, we will soon not be able to afford mealiemeal, just because of carelessness.

Assets

An asset is an item that you acquire and that has a fixed value.

Appreciation of Assets

Some things you buy can grow in value. When something grows in value after you bought it, it means that it appreciates or increases in value. The following assets usually increase in value after you have bought it:

Property - To work out how much an asset appreciates, we first determine what the growth rate for such an asset is, then we continue with working out its appreciated value.

Example:

Bheki has just bought a house for R500 000-00. He wants to know what this house will be worth in 5 years’ time.

First, he calls up a few local estate agents and asks how many properties have increased in value in this particular suburb over the past 5 years.

He gets the following answers:

Agent 1: 10%

Agent 2: 20%

Agent 3: 15% Agent 4: 12% Agent 5: 9%

He works out the average: (10 + 20 + 15 + 12 + 9) x 5 = 66 x 5 = 13.2%

Then he uses this average of 13,2% to work out the appreciation of his property in one year: R500 000 x 13,2% = R66 000

Finally he calculates this by multiplying R66 000 by the nuber of years i.e. 5 years. 66 000 x 5 = R330 000

Appreciation of Property in 5 years = R500 000 + R330 000

= R830 000

Depreciation

Depreciation occurs more frequently than appreciation. Depreciation is anything that decreases in value. Good examples of things that depreciate are:

- motor cars

- cell phones

- computers

- machinery and equipment

At the end of each financial year, companies calculate the depreciation of an item.

There are two ways of calculating depreciation, namely

- a fixed percentage of the original value (fixed method)

- a fixed percentage of the yearly depreciation amount.

Note: We only deal with the fixed instalment method.

Example:

Jack’s Hardware has to present an account of the value of their assets (i.e.

vehicles, furniture, etc.) in the business each year. After many years of experience, Peter, the bookkeeper knows that after a few years of using these items, they are worth nothing. Eventually, he writes them off. (Writing off means that something is worthless to the business).

Jack’s Hardware has a bakkie which they use for deliveries. They paid R 120 000-00 for it. Usually, they have to replace the bakkie every 5 years; otherwise, it is more in the repair shop than on the road. That means it has depreciated at a rate of 20% per year (100% + 5 = 20%)

To work out the depreciation over 5 years, we start with working it out for the first year:

Depreciation per year = 10/100 x 120000/1

= R12 000.00

Then we work out the depreciation over 5 years.

Value after 5 years = R120 000 – (5 x 12 000)

= R120 000 – R60 000

= R60 000