Page

The Income Statement

Completion requirements

View

The Income Statement (or Profit and Loss Account) is basically the organisation’s record of sales and costs for a specified period of time, usually a month, quarter or year. The bottom line of the Income Statement is the bottom line of the organisation or the net profit or loss.

The simplest equation to describe an Income Statement is...

The Income Statement does not include capital transactions such as investments, fixed assets or borrowing; however, it does include the current income and costs related to these items such as interest and depreciation.

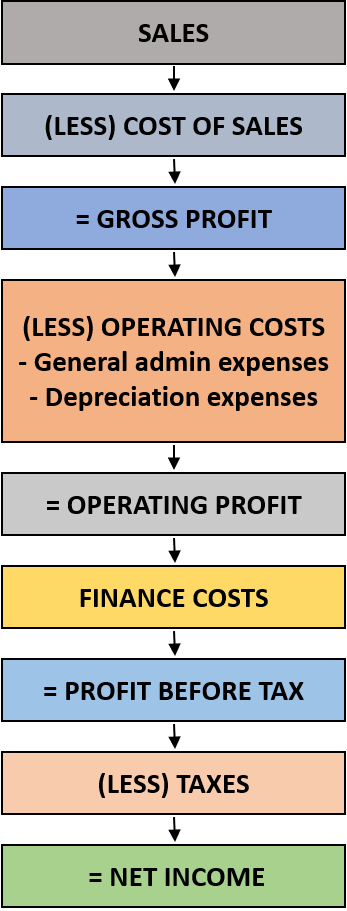

The diagram below illustrates a typical format of an Income Statement...

Income statements are not all structured exactly the same; however, this example is a typical income statement format.

Arial Trading (Pty) Ltd - Income Statement for the year ended 28 Feb 2009

|

Income: |

R |

|

Sales |

4 076 |

|

(Less) Cost of Sales |

|

|

Cost of goods sold |

(3207) |

|

Gross Profit |

869 |

|

Operating Expenses: |

|

|

General Admin/business expenses |

(227) |

|

Depreciation expenses |

(206) |

|

Total Operating Expenses |

(433) |

|

Operating Income |

436 |

|

Interest expense |

(3) |

|

Earnings before Taxes |

433 |

|

Taxes |

165 |

|

Net Income |

268 |

Let’s break down some of the main elements that could reflect on an Income Statement:-

Element of Income Statement Explanation

Income - The revenue or turnover of an organisation. The inflows form the delivery or manufacture of a product or from the rendering of a service. Income could be reflected by Sales, Revenue or Turnover.

Sales (also sometimes referred to as Revenue or Turnover) - Money is derived from selling the company’s product or service.

Cost of Sales - Includes all the spending directly associated with sales. For wholesalers and retailers, the cost of sales is essentially the prices paid to acquire the services or goods that will be resold. For manufacturers, the cost of sales is all the spending directly attributed to production (examples would include raw materials, factory overheads and wages). Cost of sales could also include research and development costs. By implication, cost of sales requires a calculation – these calculations could vary from very simple to more complexes, depending on the type of organisation. An example of a Cost of Sales calculation would be Opening Stock + Cost of Purchasing – Closing Stock. It is important to note that cost of sales does not include indirect costs (costs which cannot be directly attributed to sales and production.) Cost of sales is always a contra-entry as it is a cost.

Gross Profit - The Sales less the Cost of Sales is the Gross Profit.

Operating Expenses - All expenses related to administering the business and marketing and distributing the product or service. Operating expenses might include rent, telephone, wages, water and electricity, advertising, bank charges, insurance, fees, salaries, repairs and other expenses. Depreciation is also considered an operating expense.

Operating Profit (Or Loss) - Operating profit (or loss) is calculated by deducting Operating Expenses from Gross Profit. This is the core of the income statement.

Finance costs/Revenue or expenses/Gains or losses that are not part of the company’s normal operations. These could include interest paid on loans, interest received on deposits and investment income.

Profit (Or Loss) Before Tax - This is the operating profit (or loss) less the other revenue/expenses or gains or losses that are not part of the company’s normal operations.

Tax - Company taxes that are payable in accordance with legislation. These would be based on taxable income.

Net Profit (Or Loss) - This is the net income (or loss) after tax.

Now that you have an understanding of Income Statements, let’s do some activities using other examples of Income Statements. Ultimately, you will need to be able to interpret your own organisation’s Income Statements.

If you understand the concept of an Income Statement, you should not be afraid to tackle any kind of Income Statement, no matter how complicated. The layout of an Income Statement will follow the same basic structure (with some variations), but there may be some things in the Income Statement you have not come across before. If this is the case, then do not be afraid to research the things you do not understand. The following exercise will help to build your confidence.

Click here to view a video that explains the income statement.

Click here to learn more about the income statement and the format of the Income Statement.

Klik hier om meer te leer oor die formaat van die Inkomstestaat.