Page

Stock Control and Stock Taking

Completion requirements

View

Stock control and stock-taking are critical. Inventory management is the systematic process of stock management and relates to the goods received and dispatched, by trying to strike a balance.

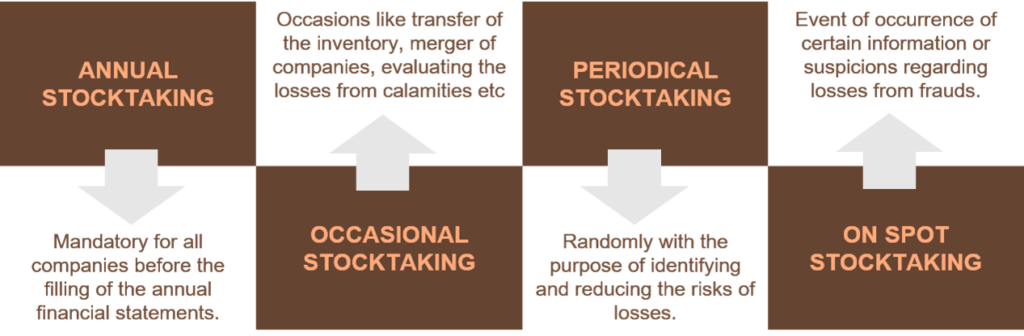

Stocktaking is:

a) The verification of actual inventory to bookkeeping records.

- Stocktaking involves the actual stock count with the aim to:

- Find the amount of stock that has been sold

- Find the amount of stock still left to be sold

- Determine stock that is missing

- Determine stock that needs to be replenished

b) Financial information on the status of inventory investment.

- The inventory is a record of stock kept. Stocktaking reveals the financial status of the stock entered into the inventory. By revealing the financial status of the inventory, the profitability of the business is scrutinized.

c) A measure of the effectiveness of inventory control procedures.

- One of the roles of inventory is to control stock as it comes in and goes out of the stockroom. Stocktaking measures how effective the control of stock through the inventory control procedure is and what the shortcomings are.

d) A method of assessing individual managers in managing assets placed at their disposal.

- Stocktaking also reveals individual managers’ ability to manage the stock at their disposal. Stocktaking is an investigation of how purchased goods, brought to the stockroom, were managed. The manager’s ability to dispose of stock, replenish stock and manage stock is revealed through stocktaking.

e) A record of inventory holdings by age groups.

- Stocktaking also reveals the ages of the goods that are still in the store and enables change of stock, replenishment and identification of stock that moves well/is stagnant.

f) An adjustment to the accounting records to complete the financial statements.

- Stocktaking enables the management to adjust the accounting records in relation to the number of goods still in-store and the number of goods sold.