Page

Gross Margin Statement

Completion requirements

View

In order to run a farm enterprise, one has to incur costs i.e. one has to buy farming requirements, and also pay for services rendered. Costs can be classified as direct costs, indirect costs, fixed and variable costs.

Definition:

The Gross margin is defined as the amount that can be calculated by the difference between enterprise gross value of the product (Gross income) and the directly allocated variable costs.

Example:

A financial budget for cotton can be calculated if the following is known:

Field size of the crop (cotton), the estimated yield and the crop value per ton or per kg. If one assumes that you would get R3.10 per kg seed cotton, and all input costs adds up to a total of R5.561, then the Gross income would be R9300 @ 300kg per ha, (calculated at the above price of R3.10 per kg) and the Gross margin would be the difference between the Gross income and the input costs.

In this case an amount of R3 739.00.

is thus very important to plan very carefully – so that you make sure that when you eventually start making a profit that you also recoup all the accumulative expenses that you had previously incurred!

Fixed Costs

Fixed costs are those costs, which cannot easily be allocated to the different enterprises or parts that make up the whole of the farm. These costs include transport, the monthly electricity account and rental or purchase payments. These costs are relevant to the farm as a whole. Fixed costs do not change if the size of the farming enterprise changes. Fixed costs will have to be paid continuously even if no production occurs.

These costs include:

- Depreciation in the value of vehicles and machinery

- Insurance premiums on fixed assets such as buildings and machinery

- Licenses

- Permanent labour

- Monthly payments for the property if money is still owed.

- Others

Variable Costs

Variable costs are costs, which can be allocated to each individual section of the farming enterprise. These are costs that are needed for production and will only be incurred when production takes place. Variable costs will change as the size of farming enterprise is changes.

Variable costs are costs that vary with the extent of production of outputs. When output increases, more labour is needed, more irrigation may be required, and more fertilizer will be used. If the enterprise reduces, production costs will also reduce. The total variable costs increase as output increases and falls as output decreases.

Variable costs include, but are not limited to the following:

- Seed to plant crops

- Purchases such as fertilizers, chemicals

- Marketing costs such as packaging, materials

- Casual labour

- Transport

- Irrigation costs for field crops

Click here to view a video that explains fixed vs. variable costs.

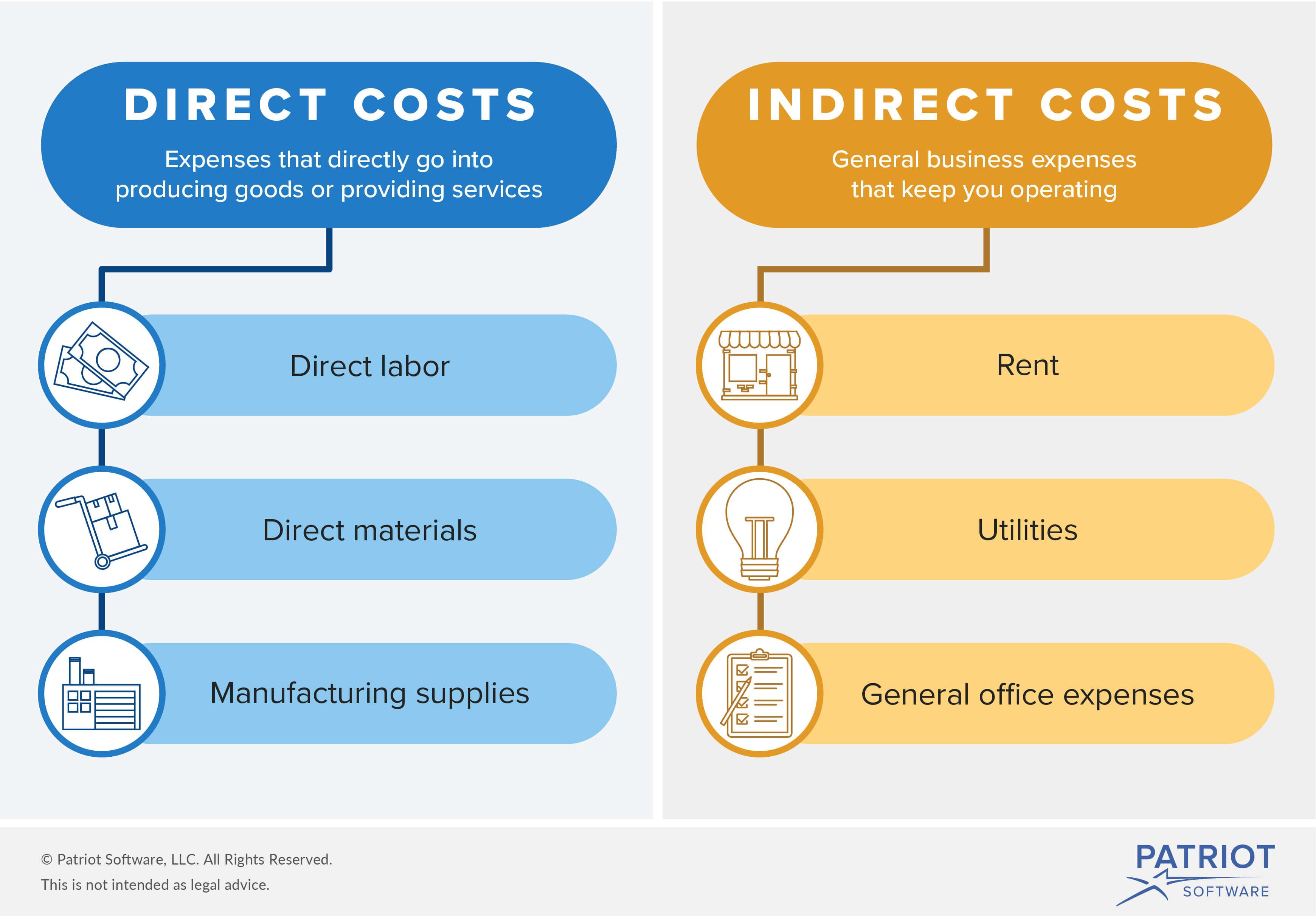

Indirect Costs

Indirect costs are those costs that are essential for the daily running of a business. They are also known as overheads or fixed costs as they remain the same irrespective of the extent of production. Included in these costs are rent, interest payments, electricity and water, municipal rates and taxes, communication costs and management costs.

Direct Costs

Direct costs are those costs that are directly linked with the production of a crop. They are also called variable costs as they vary with the output. They would include materials (fertilizer, seed) and wages paid to temporary labour.

Click here to view a video that explains direct vs. indirect costs.