Page

Manage And Control Stock Levels And Stock Records

Completion requirements

View

Managing Stocks and Stock Records

It is important that a record is kept of the stocks that are received. In most cases the stock receipt systems and stock dispatch systems are synchronised. This will help in the decision-making process of when and what should be ordered. It also allows for less reliance on stocktaking and to ensure stock levels are kept up to date. Records are needed to run an operation productively.

Guidelines on What A Record Keeping System Should Take Into Account

Guidelines on what a record keeping system should take into account:

- Minimum stock levels

- Maximum stock levels. x Standard orders and regular orders.

- Order level: - the level of stock at which a standard order must be placed before the minimum stock level is reached.

- What do you want the system to do:

- Determine the value of stock at any time

- Ensure sufficient stock at all times (confirm with the sections to achieve this)

- Compare actual stock with stock records to detect theft or out-of- date stock. (Discuss theft and abuse of stock).

- Stock analysis: - have a categorical list of all stock in the store which can be controlled by a computer data system and a backup manual system e.g.

- Dangerous materials

- Seed stock

- Animal feed

- Rations for staff

- Mechanical

- Maintenance stock

A supervisor or manager of an agricultural inputs store is responsible to ensure that inputs required on the farm are stocked correctly. It is further his/her responsibility to ensure that all the stock is kept at the levels required by the farm. To help the supervisor/manager determine these levels, stocktaking is done regularly.

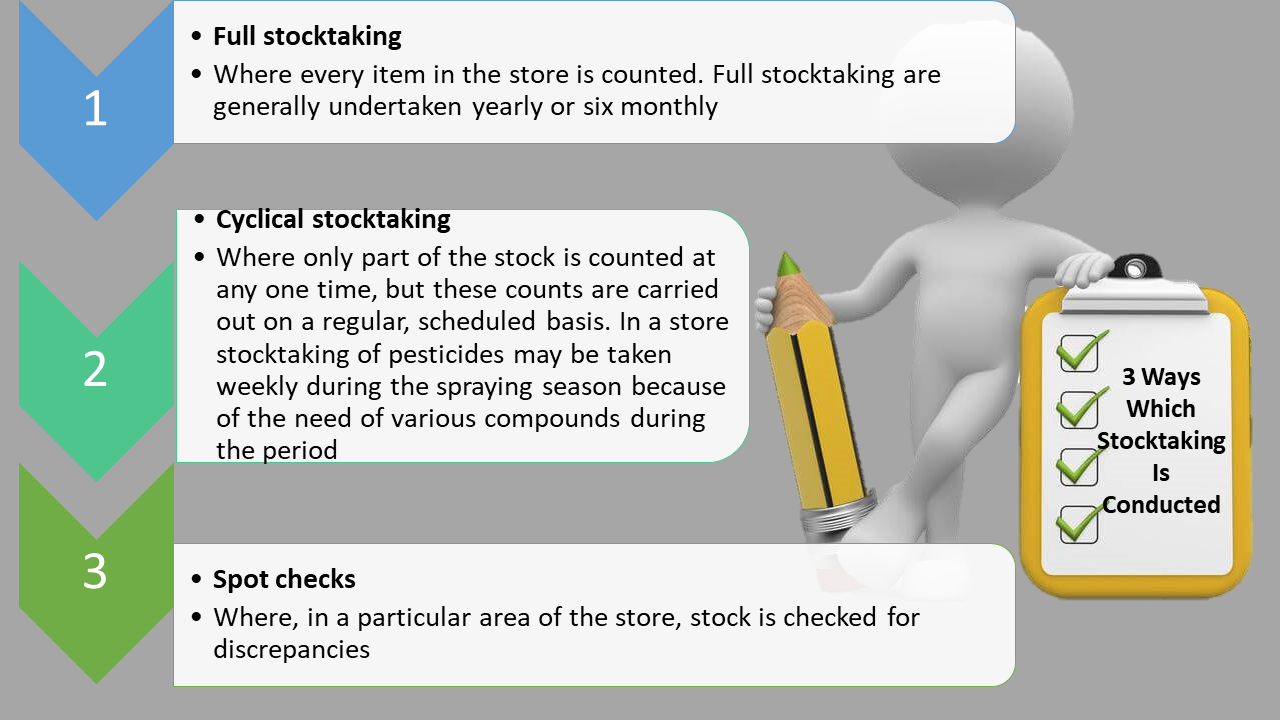

Stocktaking is the physical counting of all the stock that is in a store at a particular time. These figures generated are then compared to the stock records kept over a certain period. Conducting stocktaking allows farm personnel to accurately record what is actually in their stores.

There are three main ways that stocktaking is conducted:

Stocktaking will only be beneficial if it is carried out accurately. Stocktaking can be carried out using stock sheets or tally sheets (where stock numbers are recorded manually), or by using electronic recording equipment. These are generally portable electronic hand-held units that can record barcodes, prices and quantities.

A store supervisor or manager does not necessarily take part in stocktaking. It is the task of the manager to design and implement a stocktaking schedule. The schedule can be made up of all three types of events, but these will not be implemented simultaneously. The manager will determine the number and time of full stocktaking during a season. It may be sufficient to do a full stocktaking once during the season, whereas cyclical stocktaking may be required on a regular basis for fertilisers and pesticides during the active growing season, or periods where pest management is required. Different farms, sites and industries will have different policies and requirements concerning stocktaking. It is important that the manager implements these policies, and ensures all employees follow them.

Once stocktaking has been conducted, the manager will compare these with the actual stock records. These may be paper or electronic copies, depending on the system used on the farm.

Any discrepancies in the stock should be recorded and reported to the relevant person. Totals should be signed and then recorded so that accurate crosschecking of the actual stock counts against the recorded stock records can be conducted. If the actual stock figures do not coincide with the record system (or book stock) then this may indicate to inventory control or documenting problems.

- Problems that may arise include:

- Stock counting was incorrectly.

- Inaccurate stock recording at delivery, e.g. invoice errors, short deliveries, mistakes in recording, damaged stock, unordered stock and returns.

- Calculating mistakes when reconciling the recorded stock records.

- Mistakes in recording discounts, markdowns or waste.

- Theft by customers, staff or vendors.

If problems like these are identified, it is the responsibility of the stock controller or store manager to identify the source of the problem and implement systems that will ensure these do not re-occur. Once final stock levels for various inputs have been determined, these figures must be reported to the section supervisors. These could be the farm manager and supervisors responsible for pest management, the fertiliser programme or dairy. These people again are responsible to the management structure of the farm. It is imperative that the management structure is clear to all parties involved. The stock levels must be reported to those responsible for the use of these stocks, so that they can determine whether more stock may be required.