Page

The Balance Sheet

Completion requirements

View

A Balance Sheet is very simply a statement of position at a given date. It is like a snapshot at the close of a given day of a business.

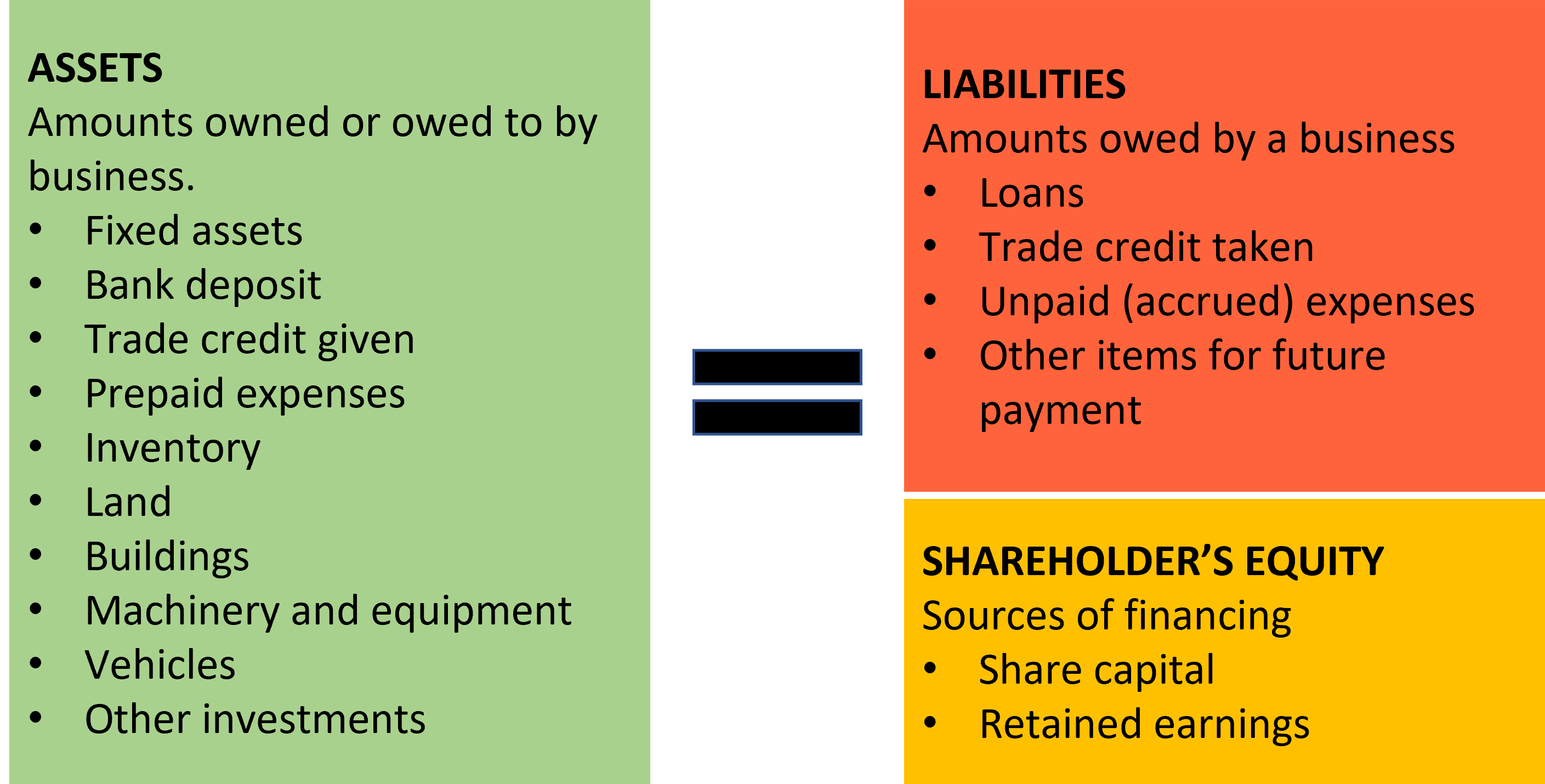

The balance sheet lists all the money owned or owed to a business (the assets) and the money owed by a business (the liabilities).

The balance sheet also includes what the owners or shareholders have put into the business (in other words the source of financing of the business) otherwise known as the shareholder’s equity.

The Balance Sheet is stated as:

Basically, you would always want to own more than you owe. So, your assets should therefore not only be equal to any liabilities (loans you may have taken), but also the actual financing that you have put into the business. Arithmetically, shareholders' equity always equals assets minus liabilities.

What Goes Into a Balance Sheet

The diagram illustrates what goes into a Balance Sheet.

Some Balance Sheets that you come across will be laid out vertically and others horizontally.

Assets and liabilities may be classified as short term (current assets and current liabilities) or as long term. Short term assets and liabilities are usually those recorded as of the current financial year, whereas long term assets and liabilities are those that are recorded over periods greater than one year.

Let’s look at the example Balance Sheet below:

Summer Trading (Pty) Ltd - Balance Sheet as at 30 September 2009

|

|

2004 |

2005 |

|

ASSETS |

R |

R |

|

Current Assets: |

|

|

|

Cash in the bank |

10 000 |

10 000 |

|

Accounts Receivable |

35 000 |

30 000 |

|

Inventory |

25 000 |

20 000 |

|

Total Current Assets |

70 000 |

60 000 |

|

Fixed Assets: |

|

|

|

Plant and machinery |

20 000 |

20 000 |

|

Less depreciation |

(12 000) |

(10 000) |

|

Land |

8 000 |

8 000 |

|

Intangible assets: |

2 000 |

1 500 |

|

Total non-current assets |

18 000 |

19 500 |

|

TOTAL ASSETS |

88 000 |

79 500 |

|

|

|

|

|

LIABILITIES |

|

|

|

Current liabilities |

|

|

|

Accounts payable |

20 000 |

15 500 |

|

Taxes payable |

5 000 |

4 000 |

|

Total current liabilities |

25 000 |

19 500 |

|

Non-current liabilities |

|

|

|

Loans – non-current |

15 000 |

10 000 |

|

Total non-current liabilities |

15 000 |

10 000 |

|

TOTAL LIABILITIES |

40 000 |

29 500 |

|

|

|

|

|

SHAREHOLDER’S EQUITY |

|

|

|

Paid-in share capital |

40 000 |

40 000 |

|

Retained earnings |

8 000 |

10 000 |

|

TOTAL SHAREHOLDER’S EQUITY |

48 000 |

50 000 |

|

LIABILITIES AND SHAREHOLDER’S EQUITY |

88 000 |

79 500 |

As you can see, total liabilities and shareholder’s equity equal total assets.

Let’s break down some of the main elements that could show on a Balance Sheet:

Assets - Economic resources that are expected to produce economic benefits for their owners. Assets can be buildings, vehicles or machinery, but they can also be patents or copyrights that provide financial advantages.

Current assets - Assets that are usually converted to cash within a period of one year. Creditors will closely monitor a firm’s current assets.

Types of current assets:

Cash and bank deposits - These are the most liquid of current assets and are used to pay the bills. (Transactional bank deposits are also regarded as cash).

Cash equivalents - These are not cash but can be converted into cash easily. (examples include securities and money market funds)

Accounts receivable - Money that should be collected from customers. Due to the fact that a lot of business is done on credit, this item often forms a significant part of the balance sheet. The notes to the accounts should show long-standing debts and provisions should be made for any bad debts. A manager should check to see if receivables are growing more quickly than sales, as this could mean trouble for the organisation.

Inventory - Inventory includes raw materials, partly completed items in progress and completed items. A manufacturing entity will have all three types of inventory, while a retail entity will only have completed items. The extent to which inventory can be turned into cash will vary and the underlying true market value of inventory will also vary. The notes to the accounts will provide more information in this regard. A manager should watch to see that inventory is not growing faster than sales as this could mean a slowdown in sales.

Pre-paid expenses - These are amounts paid in advance (for example rentals). Pre-paid expenses can be difficult to turn back into cash, but as long as the business is operating, they are considered a measure of stored value.

Long–term assets - Assets with a life of greater than one year.

Types of long-term assets:

Fixed assets - Tangible assets with a useful life greater than one year. Examples include buildings, property, equipment, machinery, production plants and vehicles. These are valued at the total acquisition cost. Fixed assets are important as they represent long term, illiquid investments. The notes to the accounts may give more detail on the fixed assets.

Depreciation or accumulated depreciation - The process of allocating the original purchase price of a fixed asset over the course of its useful life. Depreciation appears as a deduction from the original value of the fixed assets. There are different ways in which depreciation can be calculated and the manager should be aware of which method has been used. (Refer to section 4.3.1.1 for more detail on depreciation).

Intangible assets - Non-physical assets such as copyrights, franchises and patents. It is not always easy to estimate the value of an intangible asset. For some organisations, an intangible asset can prove to be very valuable. Intangible assets are usually shown separately from tangible assets or fixed assets.

Liabilities - Obligations that an organisation owes to outside parties or the rights of others to the services or money of the organisation. Examples include debts to suppliers, debts to employees and bank loans.

Current liabilities - Those obligations are usually paid within the year.

Types of current liabilities:

Accounts payable - Debts owed to suppliers for the purchase of goods and services. (for example, the company buys their goods “on account”)

Taxes payable - Any taxes that are payable in accordance with the legislation.

Short-term loans Borrowings from banks or other lenders that are repayable within 12 months.

Non-current liabilities - A debt owed over a period greater than one year is often paid in instalments. The portion to be paid off in the current year is considered a current liability.

Types of non-current liabilities:

Non-current loans - More structured kind of borrowing over periods greater than one year. Managers should note that long–term borrowing should be matched against long-term assets. If short-term borrowing is being used to finance long-term assets the organisation could be in trouble.

Provisions - Balance sheets may also include provisions or contingent liabilities (probable future costs or losses where the timing is not certain)

Shareholder's Equity - The value of a business to its owners after all of its obligations has been met. This is generally reflected by the amount of capital invested by the owners, as well as any profits re-invested.

Share capital - The book value of money raised by issuing equity or shares.

Treasury stock - The company’s holding of its own stock was repurchased in the open market.

Retained earnings - The reinvested profits or profits not distributed as dividends. Net profit less dividends are equal to retained earnings.

Now that you have an understanding of Balance Sheets, let’s do some activities using other examples of Balance Sheets. Ultimately, you will need to be able to interpret your own organisation’s Balance Sheets.

If you understand the concept of a Balance Sheet, you should not be afraid to tackle any kind of Balance Sheet, no matter how complicated. The layout of a Balance Sheet will follow the same basic structure, but there may be some things in the balance sheet you have not come across before. If this is the case, then do not be afraid to research the things you do not understand.

Click here to view a video that explains the introduction to the balance sheet.

Click here to learn more about the Balance Sheet.

Klik hier om meer te leer oor die Balansstaat.