Page

Budgeting in 7 Easy Steps

Completion requirements

View

To create a budget, you have to start by creating a picture of your financial situation. It helps to have a list of the bills that you must pay each month, as well as your pay sheets and either bank records or receipts, for the past three months.

Step 1: Determine Your Income

Begin by listing your monthly income. This should include any pay checks you receive, as well as income from other sources like:

- Child support or government benefits

- Entrepreneurial activities

- Rental income

- Investments

Step 2: List Categories of Mandatory Expenses (Living Needs)

Mandatory expenses are expenses that you must pay every month and are vital to your housing, work, or legal obligations.

These should include things like:

- Rent/home loan

- Electricity

- Water

- Food

- Medical aid

- Prescription medication not paid for by the medical aid

- Childcare

- School fees

- Transportation to and from work

- Vehicle debt

- Child support

- Insurance

You can usually identify mandatory expenses because they are fixed amounts or fixed monthly payments. If you have debt payments, they should also be included. Don't worry about assigning values yet; simply make a list of the categories.

Step 3: List Categories of Discretionary Expenses

Next, identify your discretionary expenses. These are things you can go without but often choose to spend money on. They are wants, rather than needs. They may include:

- Fitness memberships

- Clothing

- DStv/Netflix (etc.)

- Streaming subscriptions

- Eating out, entertainment

- Leisure travel

- Personal grooming

- House cleaning/domestic services/garden services

- Home décor

- Credit card payments

- Personal loan payments

- Annuity/optional retirement savings

You can also include savings goals, such as retirement accounts, investments, and annuities as discretionary expenses. There will not be immediate consequences if you scale back on these for a little while, though there may be long-term consequences if you ignore them for an extended period. Once your budget is under control, you can move these to mandatory expenses with fixed monthly contributions.

Step 4: Estimate Expenses

Once you have all your spending categories listed, it's time to assign monetary values to them. Go back through your spending history for the last three months and determine what you actually spent in each category per month. You can use your receipts or bank statements to determine what you actually spent.

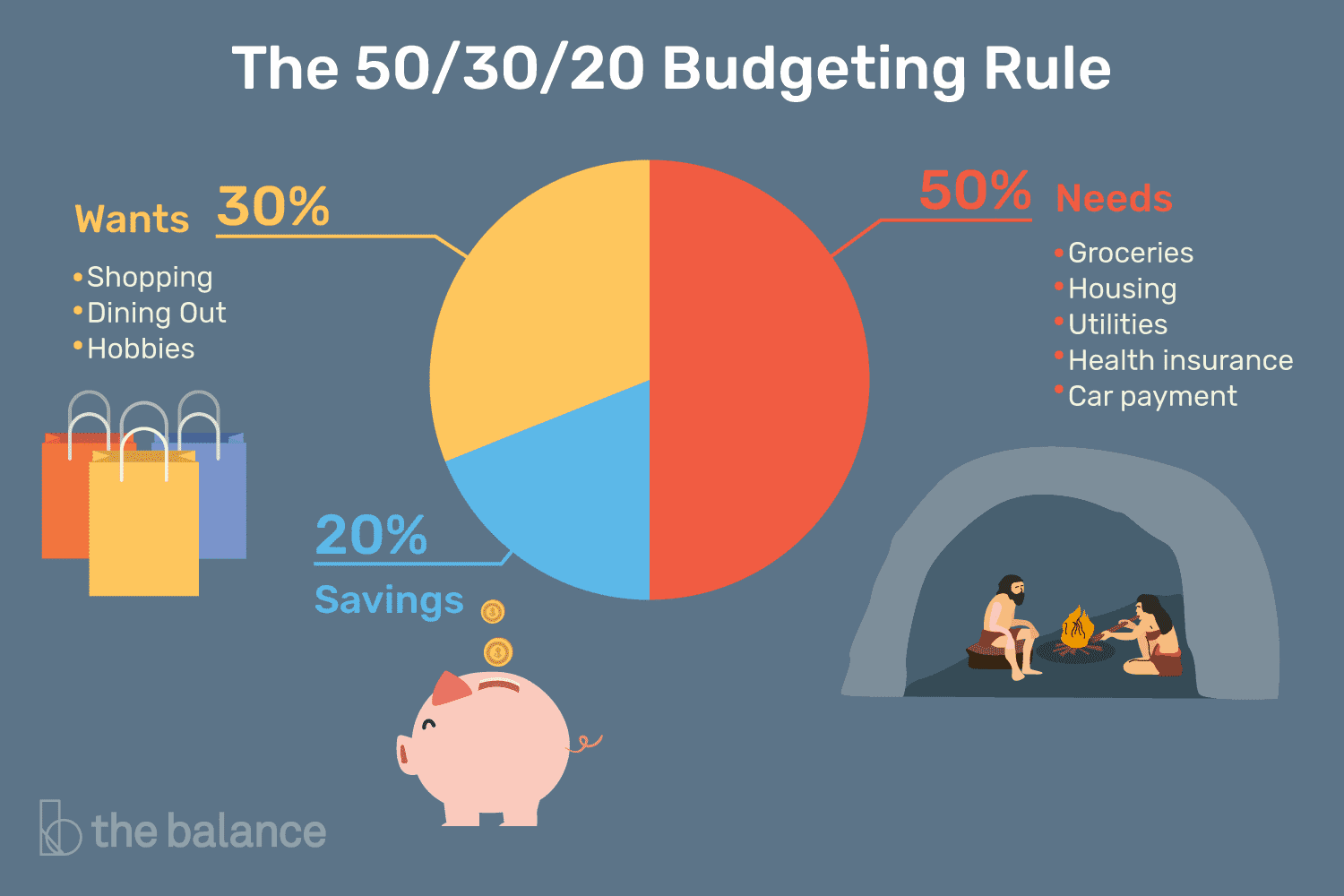

Step 5: Apply the Warren 50/20/30 Rule for Personal Financial Planning

The 50/30/20 budgeting rule requires you to track and divide your expenses into three main categories: needs, wants, and savings/debt. This reduces the amount of time you have to spend detailing your finances and allows you to focus more on the big picture instead.

Click here to view a to learn how to manage your money using the 50/30/20 rule.

Your after-tax income is what remains of your paycheck after taxes are deducted. If you're an employee with a steady income, your after-tax income should be easy to figure out (if you just look at your pay sheet). If medical aid and retirement contributions or any other deductions are deducted, just add them again.

Once you’ve figured out your after-tax income, you’ll use 50% of that amount for your needs spending, 30% for your wants spending, and 20% for debt or savings expenditures.

- According to the Warren rule, 50% of your income should go to living expenses and essentials. This includes your rent/mortgage, utilities, medical aid, insurance, vehicle down payments and things like groceries and transportation for work.

- Now, go back to your budget and figure out how much you spend each month on needs – things (like groceries, housing, utilities, health insurance, car payments, insurance and debt) you are obliged to pay e.g. the minimum amount on your credit card repayments. The amount that you spend on these things should total no more than 50% of your after-tax pay.

- 20% of your income should go to financial goals, meaning your savings, investments, and additional debt-reduction payments . Savings include annuities and pension fund contributions you make. Debt reduction has reference to debt down payment, over and above the mandatory amounts. For example, you carry a credit card balance; the minimum payment is a need and it counts toward the 50%. Anything extra is an additional debt repayment, which goes toward this 20% category.

- 30% of your income should be used for flexible spending. This is everything you buy that you want, but don’t necessarily need (like money spent on movies, travel, DStv, gym membership, cosmetics or grooming, mobile phone top ups, travel, etc.).

Step 6: Assign Spending Limits Within your Income

Now is the time to set spending limits. Expenses that you budget for should not be more than your income, otherwise you will end up in debt.

In this step you need to re-align your expenditure to the Warren principle. This may require serious rethinking and innovative action to fit expenses into the right categories.

If you have debt payments, start by budgeting for the minimum payment, then add more if you have funds left over. If you have additional money after you plan your budget, you can add it to the category for your financial goals like saving for retirement or building an emergency fund. After that, you can budget more for discretionary expenses and luxuries.

You may have to look for places to cut expenses. Start by lowering the spending limits in the discretionary section of your budget or eliminating them entirely. This may require that you cancel some of the discretionary activities such as gym membership and DStv. It could also require you to review contracts such as your cell phone or internet contracts that has luxury data cost built in.

Next, look for places where you can reduce your mandatory expenses, such as:

- Shopping around for cheaper monthly insurance premium

- Using less electricity at home

- Join a lift club to work instead of driving self

- Spending less on groceries by doing proper meal planning

- Shopping around for more affordable medical aid options

- Have the domestic worker come in twice a week as opposed to daily

If you are not making ends meet every month you could have greater expectations than you can afford. We are constantly under pressure from the media and friends to aspire to a certain lifestyle. Thus, our expectations are often greater than we can afford. It can be tempting to want all the material things we see in advertisements or that others have. But if you want to be in control of your financial affairs you need to be realistic about what you can afford. This doesn’t mean that you shouldn’t have dreams and aspirations – they are very important motivating factors in life. It means that you need to plan carefully to attain them and ensure that you don’t neglect the basics (see more about this later).

Step 7: Deposit Towards your Emergency Savings Fund

We’ve all heard the expression ‘saving for a rainy day’, which suggests a future time of need that may never come. But the reality is nobody can predict the future and by having no extra funds to pay for an unforeseen expense, you leave yourself extremely vulnerable to falling into a debt trap. Given the rising cost of living in South Africa, bank balances that run dry every month could start becoming a regular occurrence, leaving no shelter from unplanned expenses, never mind big financial emergencies.

Don’t think of the rainy-day scenario as an unlikely one. As the cost of living goes up, your ability to cover additional unplanned expenses reduces if you haven’t set aside an emergency fund. Start from your next pay cheque so you can avoid getting into debt when the next rainy day comes along.

According to Sanlam, an emergency fund should ideally contain enough savings to cover at least three times your monthly expenses. This will help you to self-fund your day-to-day expenses and meet your monthly debt obligations if you can’t earn an income. While this amount of money might seem like an unrealistic target, a good initial target would be to reduce your expenses and commit to a small amount initially allocated to the Emergency Fund. The trick is to save or invest that money as soon as you receive your salary, or even better – set up a debit order so a fixed amount goes into a separate savings account automatically. In addition, it’s important to realise that every little bit helps – anything you decide to save each month is better than nothing.

Whatever you choose to deposit in your emergency savings fund will fall within the 20% category of the Warren allocated expenses model.

Click here to download an MS Excel-based Monthly Budget Template according to the 50/30/20 principle.

Click here to download a different MS Excel-based budget template.