Page

Guidelines for Financial Stability

Completion requirements

View

Guidelines for Financial Stability During Turbulent Financial Times

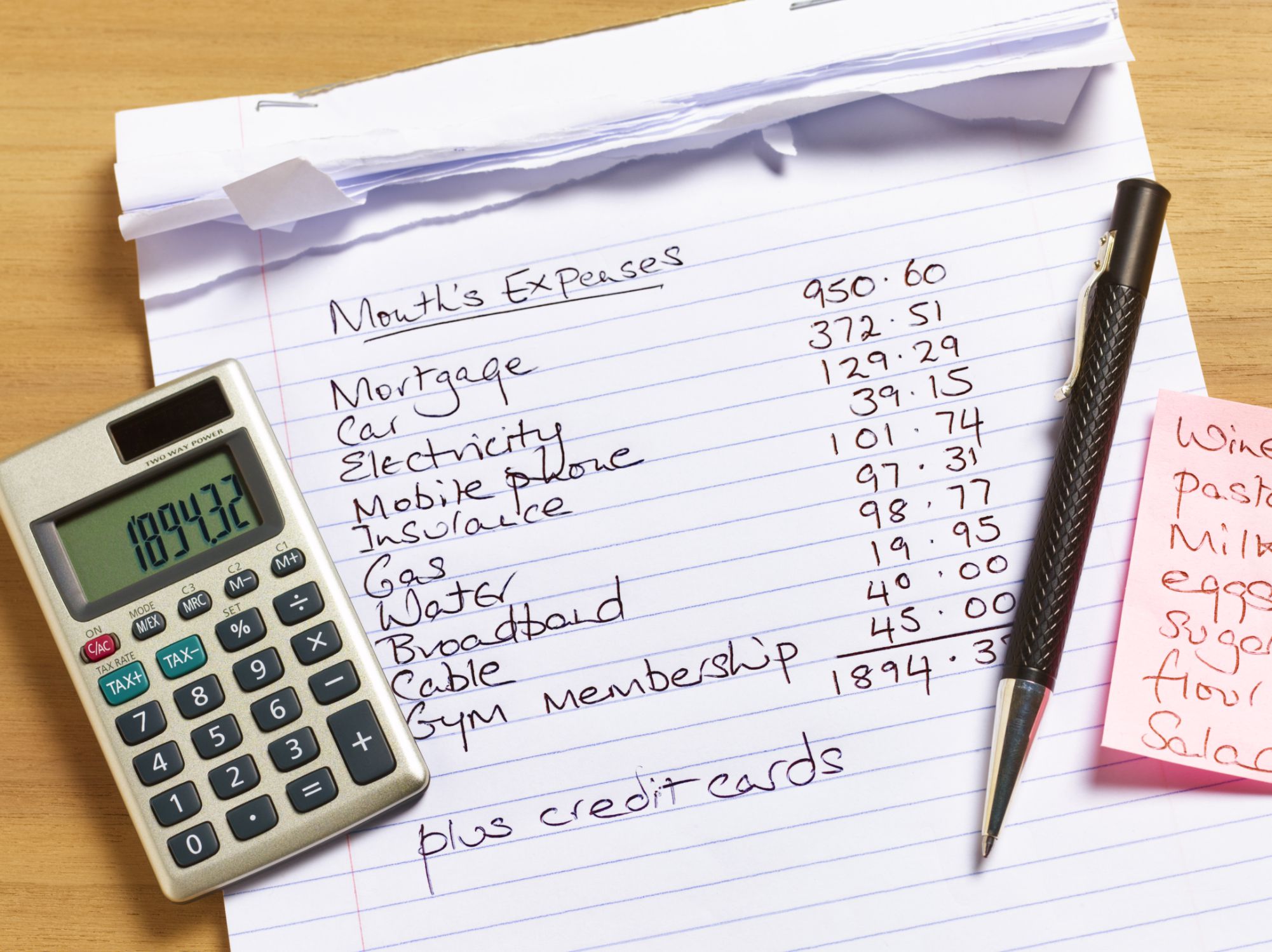

Turn Reduced Expenses into Savings

Look at your essential expenditure and how it is changing now.

Your discretionary expenditure is also likely to decrease. Before the crisis, you might have spent 30% of your income on going out, entertainment, restaurant meals, etc. Given the restrictions to leaving your home, you can generate significant savings here, up to 20% of your monthly earnings. Have a look at your previous bank statements and estimate how much money you are saving monthly on things that you no longer buy due to the crisis.

If the crisis has affected your income, you can use the savings you’ve generated to supplement it. Alternatively, that money can help you decrease your debt, build your emergency fund, or top up your savings.

If you are in a good financial position with no debt and healthy cash deposits, consider using your surplus to pay-good-forward by helping a family member/friend or a community in need, or to invest in future-proofing your finances.

Immediately re-assign these surplus funds – if not, you will spend it!

Boost Your Emergency Fund

If you’re lucky enough to have a stable income in these times, with fewer expenses, then consider boosting your emergency fund.

Avoid Excessive Buying

Shelves across the country were emptied of everyday essentials such as food and toilet paper in April and May 2020. Online shopping sites mushroomed and are extremely well-advertised on social media. The impulse to buy may be great. Before you give in to impulsive or panic buying, take stock of what you already have at home. Many of us already have well-stocked pantries that could help us survive for many weeks if not months.

Look at your current pantry and bathroom cabinet. If you already have some supplies on hand, then consider holding off on stocking up. Your wallet and your community will thank you.

Don’t Become a Co-signer to Friends or Family

While you may think you are doing yourself or someone you care about a favour, agreeing to be a co-signer on a loan is not a good idea, especially in uncertain times. The reality is that if the borrower defaults on the payments, you will be liable. If it’s your loan, you may not get as good a rate as you would have gotten if you had taken it on solo.

Don’t Take on More Debt

When in the middle of a recession, it’s definitely not a good idea to take out extra debt – with the exception being a home loan, which is used to secure an asset. You should be trying to pay off your debt as soon as possible. Learn to be patient and buy only what you need. Things you want should wait until you have the money to do so.

Don’t Accept an Adjustable Rate Mortgage if you Have a Fixed One Currently

While it may seem like a good idea to have your mortgage interest rate adapted to the lowered recession interest rates with an adjustable rate mortgage, it’s important to realise that the minute general interest rates rise, so will your mortgage. As Private Property states, “Sharp increases in interest rates may affect clients' ability to repay mortgage loans to such an extent that the financial institution has no other option but to repossess the properties concerned.” It’s important at times like these to ensure that you play it safe with a fixed interest rate – so keep it if you have it, even if it is higher than the much-reduced interest rates currently offered.

Keep Calm and Stick to your Investment Plan

One apparent impact of the economy is the increased volatility of the stock market. Although it can be tempting to panic and sell your stocks during this time of crisis, that is not a good option right now. Choosing to sell your stocks now could result in a realized loss of thousands of dollars.

It can be extremely painful to watch the value of your nest egg crumble. However, it is overwhelmingly likely that the market will recover. You should never plan on touching the money you have invested for retirement. Hold on for what looks like a wild ride ahead. Even if you expect a bumpy ride on stock, know that selling your stocks for a 20% loss is not the answer. Evaluate your investment plan and find the willpower to stick to it.

Consider Taking Advantage of Low-Interest Rates

As the feeling of uncertainty takes hold around the world, interest rates are dropping. In South Africa, the government dropped the repo rate twice and it is now at 3.75%. If you have a good credit score, then you can likely take advantage of extremely low rates for all kinds of borrowing.

If you have outstanding debt such as a mortgage or student loans, then now is the time to refinance. You could potentially save thousands throughout your loan. Although refinancing can involve quite a bit of paperwork, it will give you something to do from the comfort of your home as we tackle the weeks ahead.

Think Twice Before Spending Big

Even if your income hasn’t been affected by the pandemic, it may be a good idea to pause any major purchases right now. That’s because the future is still uncertain. Preserving your capital is everything because we don’t know how long this is going to last or what major expenses will come up.

When it comes to buying a home, for example, interest rates and mortgage rates are low right now, but that doesn’t necessarily mean home prices are at their lowest point. Typically, in market crashes, you see housing prices drop. You may have the opportunity to purchase a house at a cheaper price.

If you do buy a home now, make sure it’s a good deal and that it’s a purchase you need to make. Or, you may lose your job or incur major medical expenses, making it difficult to keep paying your new mortgage.