Page

Budget

Completion requirements

View

What Is A Budget?

A budget is a short-term financial plan, usually for a twelve-month period. On approval, a budget ultimately becomes a target and tool for management control. A budget will record the budgeted figures, the actual figures and the variance between the actual figures and the budgeted figures. Budgets should ideally not be treated as the only way to control finances, but as one of the tools in a range of measurement control.

Usually, each business unit manager/department manager will prepare a budget. These budgets are then aggregated to form the overall budget for the organisation.

Budgets should be consistent across the organisation, prepared using the same headings expectations and assumptions so that they can be aggregated into the final budget. For example, manufacturing budgets need to be aligned with what sales are budgeting. Also, ensure that interest rates or exchange rates are being used consistently across different business units.

Where Do Budgets Fit In?

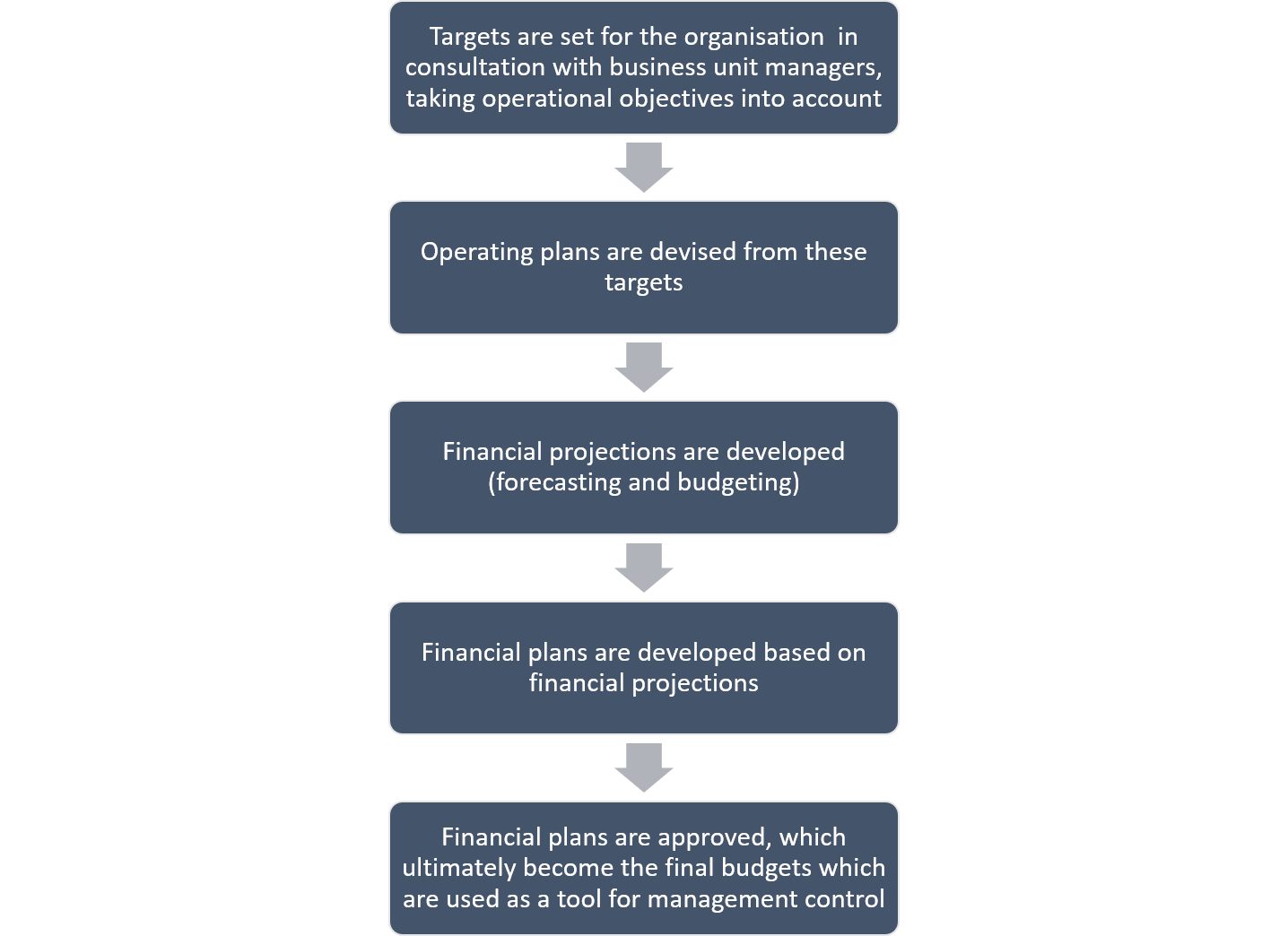

There is quite a bit of overlap between the budgeting process and the forecasting process. The following diagram illustrates, generally speaking, where budgets fit in:

Click here to view a video that explains the difference between budgeting and forecasting.

Business unit managers are usually required to report on their progress against their budget each month. This is done by comparing actual spending against budgeted targets. At the end of the budget year, organisations usually conduct more comprehensive comparisons. Often organisations use end of budget year comparisons as performance measurements to reward or “punish” employees, however a better approach would be to incorporate the budget measurement tools with other forms of measurement to reduce the risk of turning budgets into harsh, bureaucratic management tools.

Figures from budgets should be evaluated in conjunction with other organisational elements. These include customer perceptions, strength of processes and ability to innovate. This is sometimes referred to as a “Balanced Scorecard Approach.”