Page

Items That Makeup Expenditure In A Business Unit

Completion requirements

View

Expenses are those costs necessary to run the business efficiently. Expenses usually arise on an ongoing basis, such as monthly or annually.

These expenses would include the purchases of goods or services for use by the business within the financial year. Examples are as follows:

- Goods for resale

- Salaries and wages

- Repairs

- Electricity and Water

- Petrol

- Professional fees

We must remember that for every item or service sold by a business there is an expense incurred. If we look at the above statement, we can see exactly what the company has paid for.

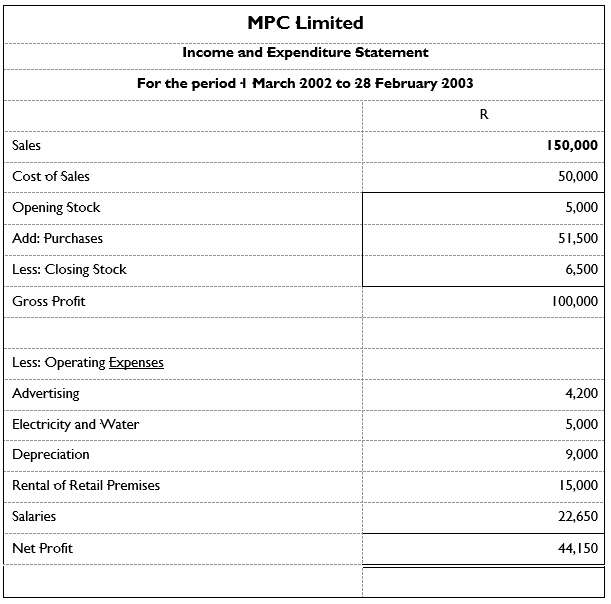

Let’s again look at the Income and Expenditure Statement of MPC Limited and see if we can identify the company’s expenses:

You will notice in the above statement that there is an amount of R50 000 for Cost of Sales. The Cost of Sales calculation is made up of Opening Stock Add Purchases Less Closing Stock and is calculated and subtracted from sales to give you the Gross Profit.

The above-mentioned statement lists expenses as follows:

Cost of Sales

These would include:

Opening stock: the amount of stock the business has at the beginning of the accounting period.

Purchases – these would be items required, such as, till rolls and other stationery, cleaning equipment etc. as well as raw materials or goods bought at cost price.

Operating Expenses

These would include:

Rental of the premises: (unless the owner of the business has purchased the property).

Advertising costs: the advertising could be in the form of a newspaper or TV or the use of the large billboards that we see as we travel.

Depreciation: assets such as vehicles and machinery such as a photocopier devalue in time.

Salaries: these would be the salaries of all the people involved in the business, but not of the owner.

The manufacturer would have the following expenses in order to manufacture and then sell his finished product:

Raw Materials: These are the basic components of his saleable product.

Vehicle expenses: These are not the costs related to the purchasing of the vehicles, but rather the cost of running them e.g. petrol, maintenance and repairs, tyre replacement etc.

Salaries and Wages: All employees involved in the purchasing of raw materials, manufacturing of the product, administrative processes and sales need to be paid.

Advertising: The owner of the business would not be able to sell his product effectively without advertising. This costs money and would therefore be considered an expense.

Insurance: Insurance costs could include: Public Liability; Workman’s Compensation; Life Cover; cover against fire & theft.

Stationery: Letterheads, envelopes, pens, pencils and all other stationery that would be required for the office.

Rent: The rent for the premises.

Electricity and Water: Payment for electricity and water for the premises.

Telephone: The telephone account would need to be paid.

There could be many more expenses that have not been listed above that a business would have to pay for.

All the expenses that have been listed must be calculated and added to the company’s budget. It should be remembered that actual expenses are often more than a business will budget for. So, to ensure an accurate forecast of expenses it is necessary for a business to focus on the types and amounts of expenditure. Check with the previous year’s expenditure to prevent leaving out costs from this year’s budget.

Let’s have a look at the different types of expenditure that need to be considered for a budget:

|

TYPE: |

EXAMPLES: |

|

Ongoing Specific Costs |

Raw material and component parts, bought-in services, goods for resale, labour and wages, after-sales support and service. |

|

Ongoing Shared Costs |

Rent, rates, utilities, insurance, repairs, infrastructure, finance charges, postage, stationery, advertising, telephone, transport and professional fees. |

|

Once Off Start-up Costs |

Drawings, pre-trading items, set-up costs, specifications, production lines, sales and marketing literature and employment and re-training costs. |

|

Once-off Capital Non-revenue Costs |

Tangible assets such as buildings, plants and equipment. Office machinery, fixtures and fittings, motor vehicles and intangible assets such as goodwill, brands and intellectual property. |

As you can see from the above table, there are four main types of expenditure that need to be considered when preparing a budget.

On-going specific costs are costs that are driven by particular products and services.

On-going shared costs are those that are shared by the whole organisation and are incurred by most organisations all the time on a routine basis. They can be easily estimated and controlled.

Start-up costs are those that are incurred when starting or growing a new operation. These costs will vary each time.

Capital or non-revenue costs are one-off items. They are usually harder to estimate because they do not happen often. When they do, they are likely to be different each time.