Page

The Cash Flow Budget And Statement

Completion requirements

View

Cash flow is the money needed to run your company on a day-to-day basis. This is the money available after all the expected expenses have been covered, for unexpected expenses.

Cash flow statements are a tool that reflects the sources from which funds are generated during the accounting period as well as the purpose for which these were used.

The cash flow statements must be compiled for one year or at least until positive cash flow is achieved if not attained within the first year.

The most important feature of a cash flow budget is that only cash expenses and cash income are indicated at the estimated time of payment or receipt.

The cash flow statement reflects the source from which funds were generated during the accounting period. Cash flow is an important consideration when it comes to financing a business. The bank and monthly bank balance are important elements of a cash flow statement. A cash flow statement consists of three components: income, expenditure and bank balance.

Income consists of operating income, capital income and cash income.

Expenditure is classified as operating expenditure, capital expenditure and debt repayment.

Shortfall/surplus is calculated by deducting total expenditure from the total income.

The various components of a cash flow budget statement are:

|

Opening Cash Balance |

Farm Income |

|

Capital income |

|

|

Nonfarm Income |

|

|

Farm Operating Expenses |

Fertilizers |

|

Leases or rental |

|

|

Sprays |

|

|

Wages |

|

|

Repairs |

|

|

Capital Expenditure |

Machinery |

|

Livestock |

|

|

Other Expenditures |

Income statement |

|

Living wages |

|

|

Scheduled Debt Payment |

Interest |

|

Redemption |

|

|

Total cash outflow |

|

|

Closing cash balance |

The Need For The Twelve Month Cash Flow Budget

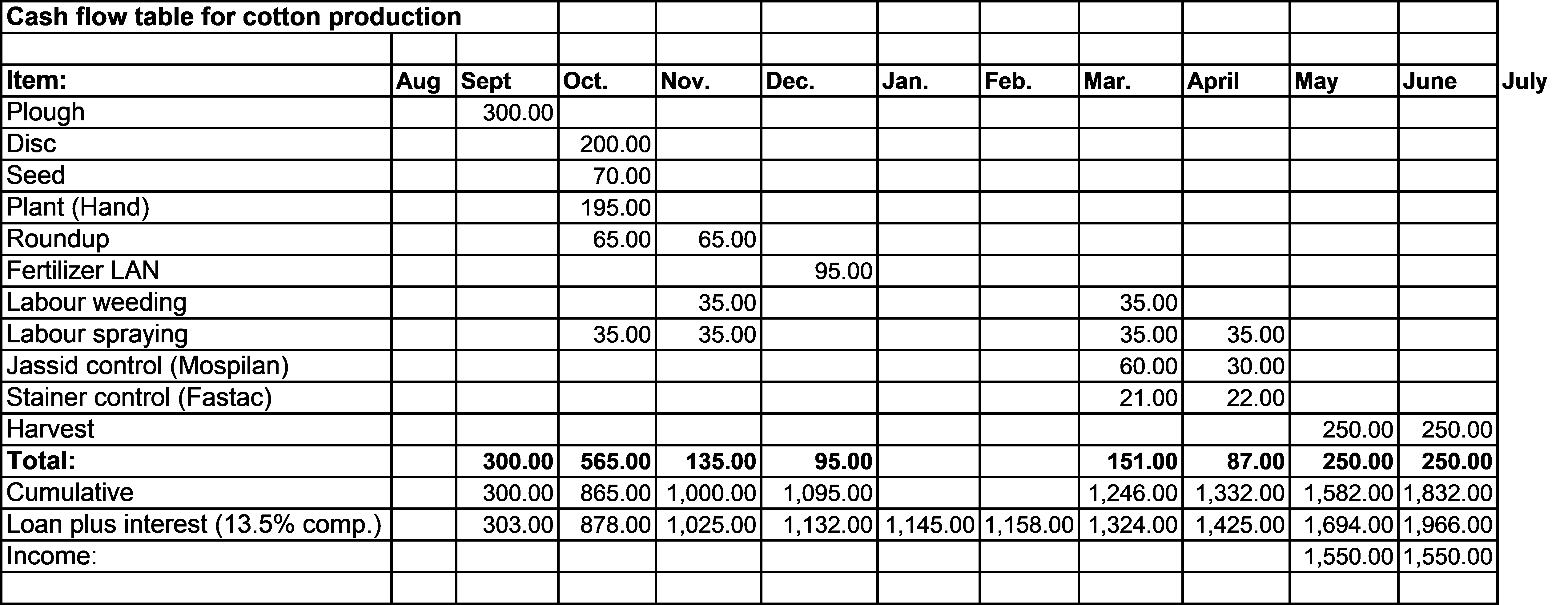

In order to understand a cash flow budget, it is necessary for a farmer to understand which activities take place during the season, and the associated costs to complete these activities successfully. For example, cotton is a cash crop. In order to set up a cash flow budget the farmer must have a cultivation programme in place as the crop will need attention (insecticides, fertilizers, picking, ext.) at different growing stages, and therefore, cash must be available for every event according to the programme arranged beforehand.

Example:

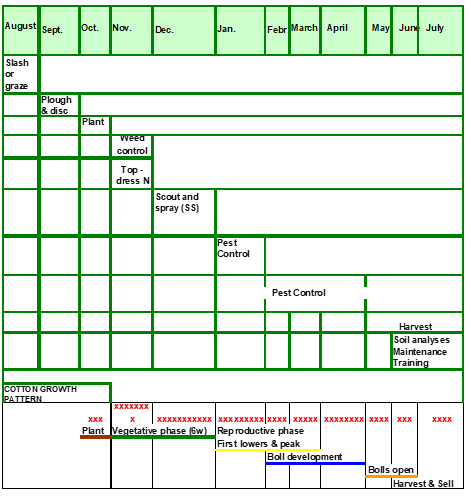

A Critical Pathway Of Activities For Cotton Production

The farmer should have a good knowledge of:

- Length of the crop season.

- In which months every activity should take place to produce the crop.

- Plant development for each crop cultivated should be clear, in order to express good pest control and optimum yields.

- The farmer should set up an outline of the crop size he would like to produce.

- He/she should be able to recognize the infrastructure available

- Which inputs are needed, financially and support services?

- Have a clear comprehension of the available workforce (labour)

- When a critical programme has been drawn up as above, the learner can compile cash flow statements. These are probably the most important aspect of the financial management of a farming business. Many farming based businesses currently experience cash flow related problems. A 12-month cash flow budget predicts an estimate of cash needed for a year.

- A Cash flow budget is a budget that breaks the yearly cash flow into twelve-month segments. This allows for greater control of the flow of cash.

- A cash flow statement presents the source and use of the funds of the enterprise according to operating activities, investing activities and financing activities.

- Operating activities describes the cash received for the product and cash payments made for production costs.

- Investing activities describes the purchasing of new equipment or expanding the operation.

- Financing activities describes the repayment of long-term loans.

Example: